How the All-In-One Loan Works (and Why It’s Smarter Than a Traditional Mortgage)

If you’ve ever looked at your mortgage statement and wondered why the balance barely moves, you’re not alone. Traditional mortgages are structured to benefit the bank—not you. The All-In-One Loan™ (AIO) flips that system, giving you a smarter, faster way to pay off your home while keeping full control of your money.

Let’s break down how it works—and why it could be the most powerful financial tool you’ve never heard of.

Traditional Mortgages: Built for the Bank

Here’s how the math works against you:

You borrow a lump sum.

You repay it over 30 years with fixed monthly payments.

In the early years, up to 70–80% of each payment goes to interest, not principal.

It’s called amortization, and it’s designed so that banks earn most of their profit upfront.

That’s why even with a “low” 3% rate, you could pay six figures in interest over time.

📊 Example:

A $400,000 mortgage at 3% = nearly $207,000 in total interest over 30 years.

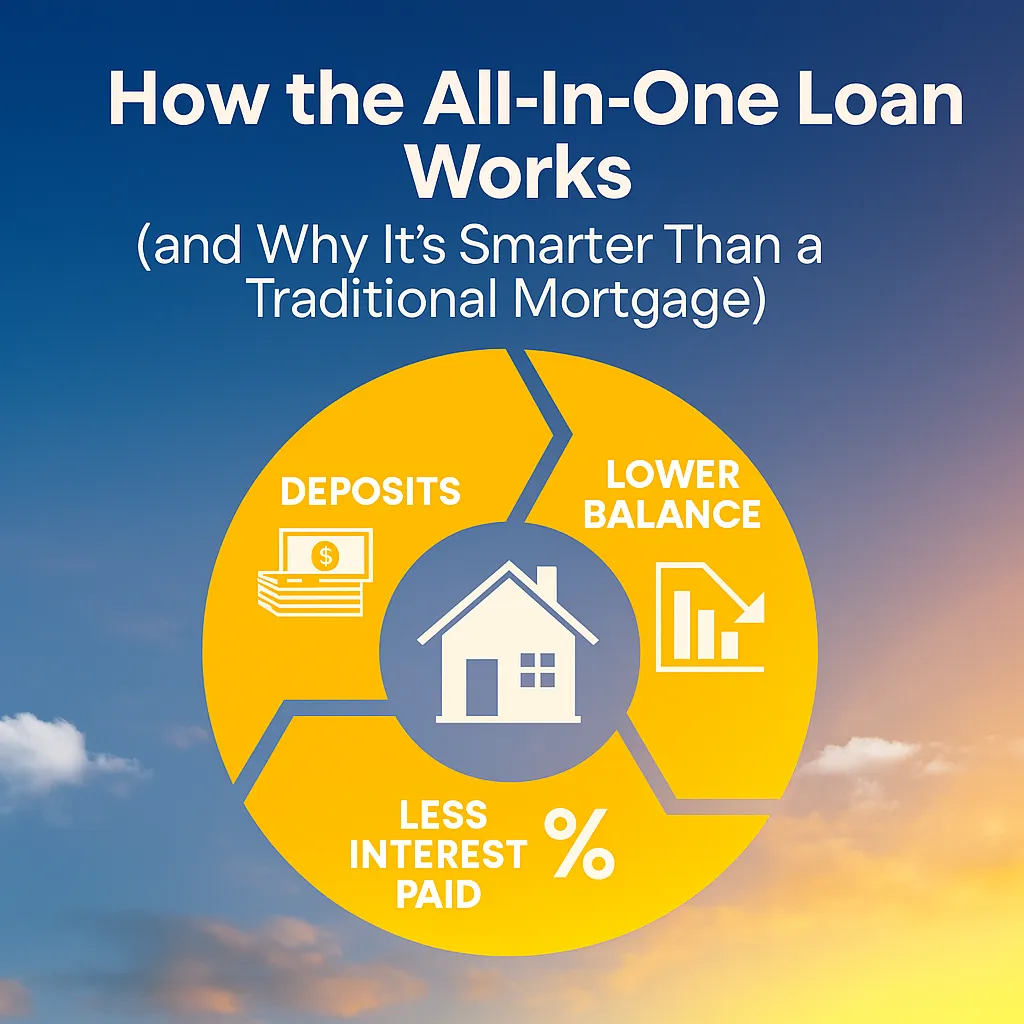

The All-In-One Loan™: How It Works

The AIO combines your mortgage + checking + savings into one account.

Here’s what makes it revolutionary:

Your income deposits directly lower your loan balance.

Every dollar you earn immediately reduces what you owe.Interest is calculated daily—not monthly.

So even short-term balance reductions save you real money.You still have full access to your cash.

You can withdraw anytime for expenses, investments, or emergencies.

In short, your money is no longer sitting idle—it’s working for you 24/7.

💡 Think of it like this:

Instead of your checking account earning 0.5% interest while your mortgage costs 6%, the AIO lets your cash offset that 6% daily.

Real-World Example

Let’s say you have a $400,000 balance and $10,000 of monthly income.

With a traditional mortgage: that $10,000 sits in checking until bills are paid—earning nothing.

With the AIO: the $10,000 immediately reduces your mortgage balance, saving daily interest until you spend it.

Over a year, that simple shift can save thousands in interest—and shorten your payoff timeline by 10–15 years.

The AIO isn’t just another loan—it’s a financial ecosystem that makes your money work like compound interest in reverse.

Why It Outperforms Traditional Loans

1. Faster Payoff – Many borrowers pay off their homes in 10–15 years instead of 30.

2. Massive Interest Savings – You could save $100K+ in lifetime interest.

3. Full Flexibility – You can access your money anytime, unlike with extra payments on a fixed loan.

4. Smarter Cash Flow Management – Your income becomes your biggest debt-reduction tool.

The AIO isn’t just a mortgage—it’s a cash-flow engine that works for you.

Why It Outperforms Traditional Loans

1. Faster Payoff – Many borrowers pay off their homes in 10–15 years instead of 30.

2. Massive Interest Savings – You could save $100K+ in lifetime interest.

3. Full Flexibility – You can access your money anytime, unlike with extra payments on a fixed loan.

4. Smarter Cash Flow Management – Your income becomes your biggest debt-reduction tool.

The AIO isn’t just a mortgage—it’s a cash-flow engine that works for you.

Who It’s Best For

This loan structure works best for financially disciplined homeowners who:

✔ Have consistent income and positive cash flow

✔ Spend less than they earn

✔ Want long-term financial freedom and liquidity

If you’re living paycheck-to-paycheck, the AIO might not be ideal—it rewards consistency and control.

The Takeaway

The All-In-One Loan™ changes everything we’ve been taught about mortgages.

It’s not about getting the lowest rate—it’s about using your money smarter.

If you want to:

Pay off your home faster,

Save thousands in interest,

And stay in control of your cash flow...

Then it’s time to look beyond traditional lending.