Why the All-In-One Loan Has No Due Date

If you’ve ever heard that the All-In-One Loan™ doesn’t have a “due date,” your first thought might be: Wait—what? How does that even work?

After all, every other mortgage you’ve ever seen comes with one thing for sure—a fixed payment due every month.

But the All-In-One Loan isn’t built like a traditional mortgage. It’s built around cash flow, not fixed schedules.

Here’s why that’s a good thing—and how it gives you more control over your money.

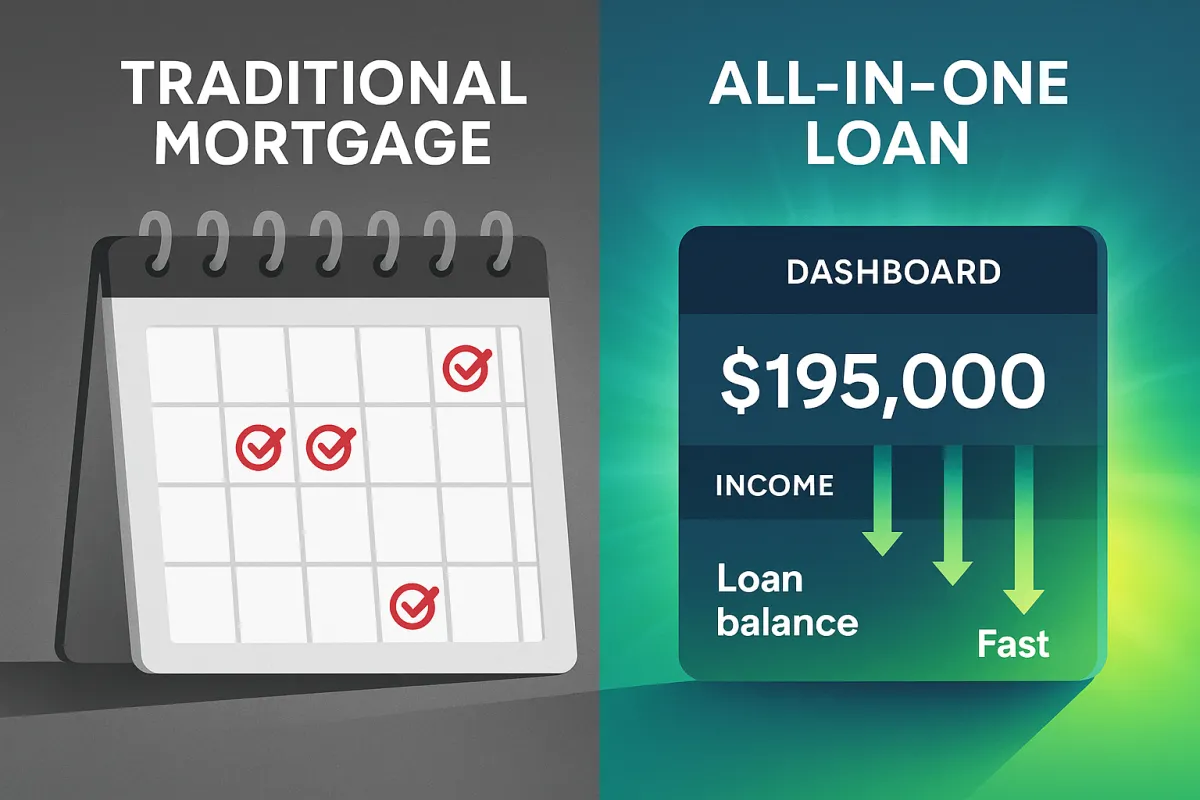

Traditional Mortgages Are Built on Payment Cycles

In a conventional loan, you borrow a lump sum and agree to pay it back over a set term (usually 30 years).

Your lender then divides that repayment into monthly installments, which include both principal and interest.

The key thing?

The interest is front-loaded, which means most of your early payments go straight to the bank, not to your balance.

📅 Example:

Even after 5 years of payments, you might have barely touched your original loan balance.

That’s because traditional loans are structured to make you commit to long-term, fixed payments—maximizing the bank’s profit and minimizing your flexibility.

The All-In-One Loan Works Differently

The All-In-One Loan merges your mortgage, checking, and savings into one account.

That means every time money flows in (paychecks, bonuses, rental income, etc.), it immediately reduces your loan balance.

💡 Here’s the secret:

Interest is calculated daily, not monthly.

So even if your money sits in the account for just a few days before bills go out, it still lowers your principal and reduces interest.

That’s why there’s no “due payment.”

The system automatically adjusts based on your income and expenses.

Instead of paying on a fixed date every month, you’re paying interest in real time as your balance fluctuates. Your money never sits idle—it’s always working for you.

Why This Structure Works in Your Favor

1. No Missed Payments

Because there’s no “due date,” you can’t be late. Your deposits naturally service the loan daily.

2. More Control Over Cash Flow

You decide when and how to apply funds—your money isn’t trapped inside the mortgage.

3. Daily Savings Add Up

Even a few days of lower balance can shave thousands off total interest over time.

4. Automatic Principal Reduction

Every deposit helps pay down your balance, automatically and efficiently.

Example: How It Plays Out

Let’s say you have:

$400,000 loan balance

$10,000 monthly income

$8,000 in monthly expenses

With a traditional mortgage, your payment is fixed—say $2,200 a month—most of which goes to interest.

Your paycheck sits in checking, doing nothing, while your debt collects interest.

With the AIO Loan, your $10,000 paycheck immediately reduces your mortgage balance to $390,000.

Interest is charged only on that reduced amount.

When you pay bills throughout the month, the balance rises and falls—but every day your income sits there, it’s saving you money.

That’s how AIO borrowers can pay off a 30-year loan in as little as 10–15 years—without increasing payments.

The Freedom of No Due Date

“No due date” doesn’t mean “no discipline.”

It means freedom—the freedom to let your cash flow work for you, not against you.

You’re no longer stuck in a rigid payment schedule that favors the bank.

You’re in control.

And the best part?

You can still access your funds anytime. If an emergency, investment, or opportunity comes up, your equity isn’t trapped—you can use it instantly.

When It Might Not Be the Right Fit

The All-In-One Loan works best for financially disciplined borrowers who:

Have stable, positive cash flow

Spend less than they earn

Want to save interest and maintain liquidity

If you live paycheck to paycheck or rely on credit frequently, a traditional fixed loan might still suit you better.

Key Takeaway

The All-In-One Loan isn’t just a mortgage—it’s a money management system that rewards you for being smart with your income.

It removes the burden of “monthly due dates” and replaces it with real-time financial control.

You’re not just making payments—you’re accelerating your path to debt freedom.

Conclusion

No due date doesn’t mean no responsibility—it means no limits.

The All-In-One Loan gives you total control of your finances, making your income work harder, your debt shrink faster, and your peace of mind last longer.